1. Overview

When a search action is conducted by the Income-tax Department, under the provisions of section 132/132A on or after 1st Sept 2024, the assessment is required to be made in accordance with the provisions of Section 158BC or 158BC r.w.s 158BD. These provisions require the assessments to be made under the block assessment covering the “block period”, comprising previous years relevant to six assessment years preceding the previous year in which the search was initiated under section 132 or any requisition was made under section 132A and also includes the period starting from the 1st day of April of the previous year in which search was initiated or requisition was made and ending on the date of the execution of the last of the authorisations for such search or such requisition. The return of income for such ‘block period’ is required to be filed in ITR-B.

Form ITR-B has been notified through CBDT Notification No. 30/2025 dated 7th April, 2025, for this purpose.

2. Who is required to file ITR-B?

ITR-B is required to be filed under Section 158BC or 158BC r.w.s 158BD.

ITR-B is required to be filed by:

Any entity or person who has been subjected to:

- A search under Section 132, or

- A requisition of books of accounts/assets under Section 132A of the Income Tax Act, where-

- the search or requisition has been conducted on or after 1st September 2024, and

- the Assessing Officer issues a notice under Section 158BC or 158BC r.w.s 158BD, requiring them to file a block assessment return.

.

3. Due date for filing ITR-B?

The due date for filing Form ITR-B is the date specified in the notice issued by the Income Tax Department following a search or requisition action.

4. Prerequisites for filing ITR-B?

a.) Notice for block assessment received under Section 158BC or 158BC r.w.s 158BD.

b.) PAN and e Filing account (login credentials).

c.) Details of returns of income filed for the period falling under the Block period.

d.) Details of undisclosed income and assets during the block period:

• Income heads (salary, B&P, house property, capital gains, others).

• Assets: cash, bullion, jewellery, digital assets, foreign assets, etc.

e.) TDS/TCS credit information, if any, which remains unclaimed for the AYs covered in the relevant block period.

f.) Tax computation, including interest applicable, if any.

5. What is the process of filing ITR-B?

Step by Step process of filing ITR-B:

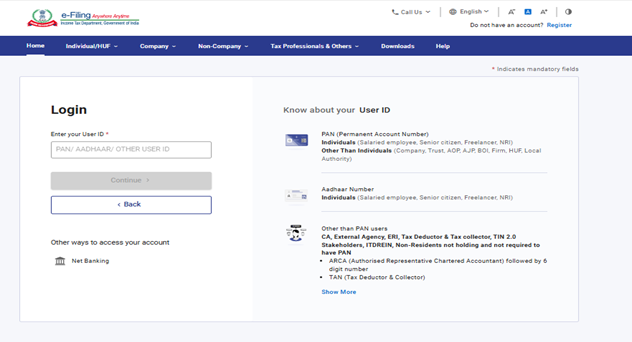

Step-1: Log in to the e-Filing portal.

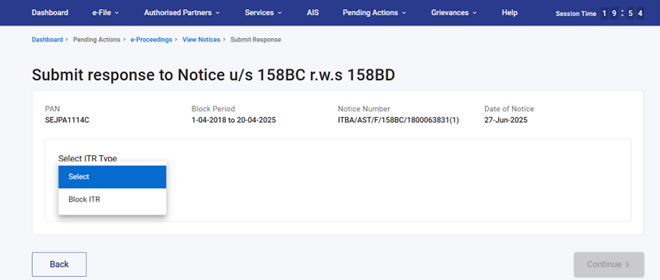

Step-2: Go to e-Proceedings and click on submit to notice u/s 158BC or 158BC r.w.s 158BD and select Form - Block ITR.

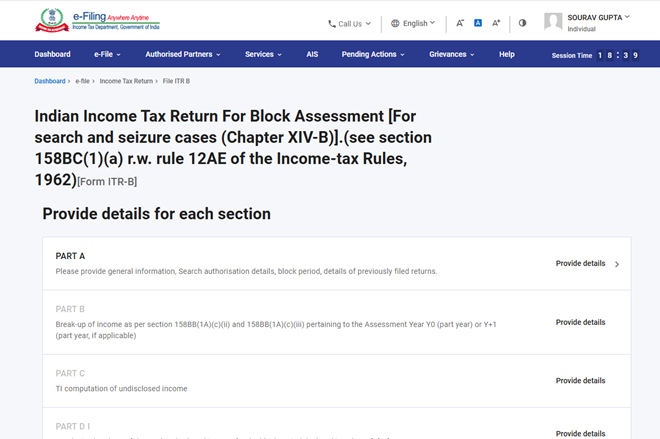

Step-3: Fill in all the required details, such as information about the undisclosed income found during the search.

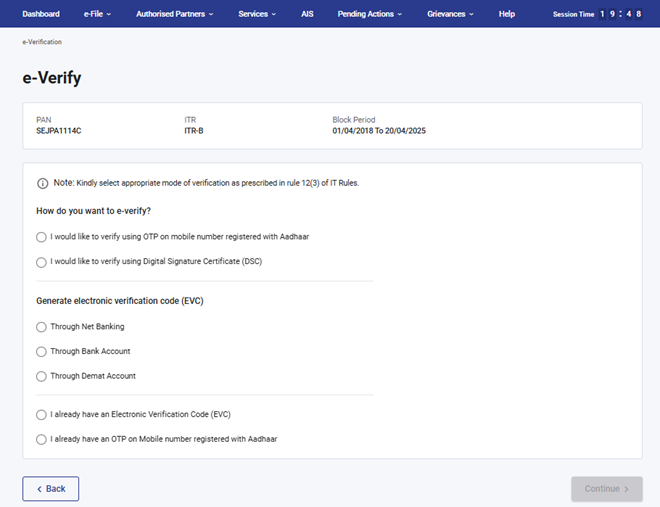

Step-4: Submit the return online, using either your digital signature or EVC (Electronic Verification Code), whichever applies to you.

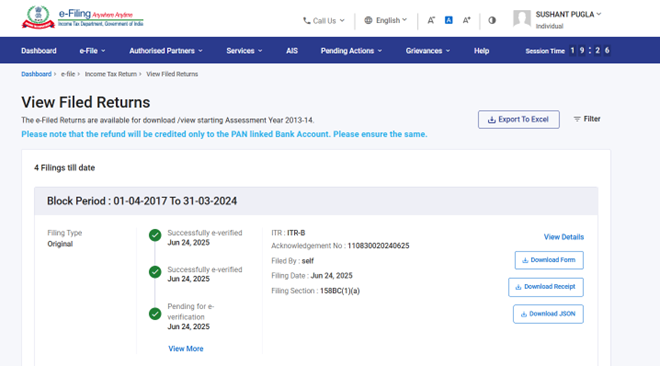

Step-5: To view the submitted return you can navigate to e-file -> Income Tax Return -> View Filed Return.

Glossary

| Acronym/Abbreviation | Description/Full Form |

| ITR | Income Tax Returns |

| DSC | Digital Signature Certificate |

| AY | Assessment Year |

| PY | Previous Year |

| FY | Financial Year |