File ITR-4 (Sugam) Online User Manual

1. Overview

The filing of ITR-4 service is available to registered users on the e-filing portal and through accessing the offline utility. This service enables individual taxpayers, HUFs, and firms (other than LLPs) to file ITR-4 online on the e-filing portal.

This user manual covers the step-by-step process for filing ITR-4 through the online mode.

2. Prerequisites for availing this service

| General |

|

| Others |

|

3. About the Form

3.1 Purpose

Income Tax Return is the form in which taxpayers furnish information about income and tax thereon to the Income Tax Department on annual basis. Form ITR-4 can be used by Resident Individuals, HUFs, and firms (other than LLPs) fulfilling criteria as per 3.2 below for filing their Income Tax Return in old or new tax regime.

3.2 Who can use it?

ITR-4 can be filed by a Resident individuals /HUF/Partnership firm who fulfill the following conditions:

• Having Business or Professional Income

• Income from business calculated under Section 44AD or 44AE

• Income from profession calculated under Section 44ADA

• Long-term capital gains u/s 112 A up to Rs. 1.25 lakhs (having no brought-forward or carry-forward capital loss)

• Should not have income from more than two house property

Please Note:

ITR-4 Form is not for an individual who is either Director in a company or has invested in unlisted

equity shares or if income-tax is deferred on ESOP or has agricultural income more than Rs. 5000 or has assets (including financial interest in any entity) located outside India.

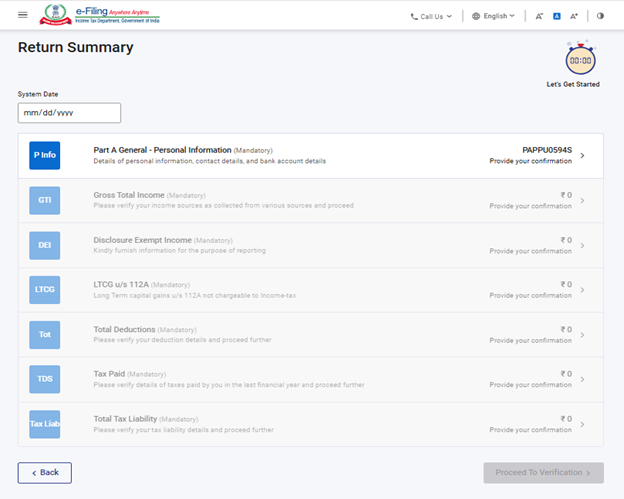

4. Form at a Glance

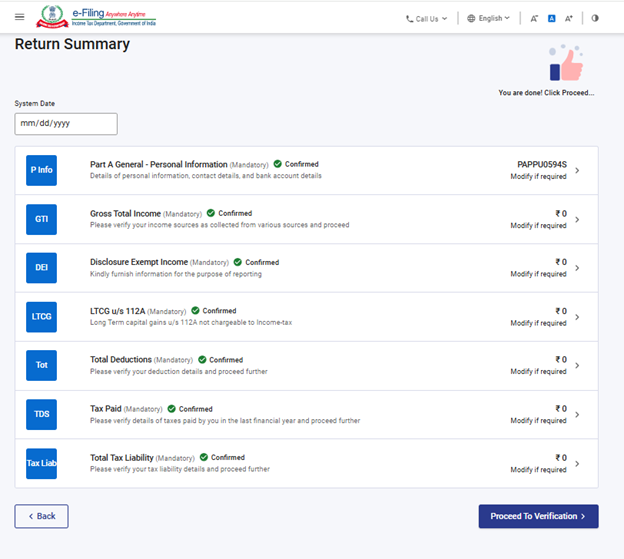

ITR-4 has Seven sections that you need to fill before submitting the form in online mode and a preview page where you can validate all your details filled. The sections are as follows:

1. Personal Information

2. Gross Total Income

3. Disclosures and Exempt Income

4. Long term Capital Gains u/s 112 A

5. Total Deductions

6. Taxes Paid

7. Total Tax Liability

Here is a quick tour of the various sections of ITR-4:

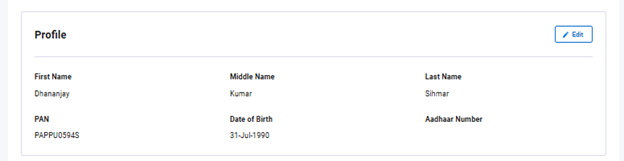

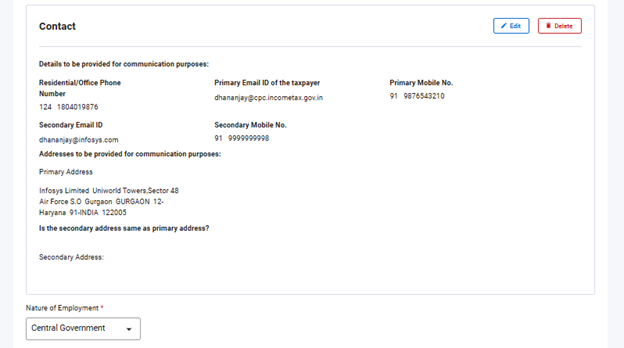

4.1 Personal Information

In the Personal Information section of the ITR, you need to verify the data which is auto-filled from your e-filing profile. You will not be able to edit some of your personal data directly in the ITR form. However, you can make the necessary changes by going to your e-filing profile. You can edit your Profile Details (Only Aadhaar number can be entered), contact details, filing type details, authorized representative, partner details (if applicable), and bank details in your e-filing profile.

Profile details:

Contact Details:

Filing Type Details:

Note:

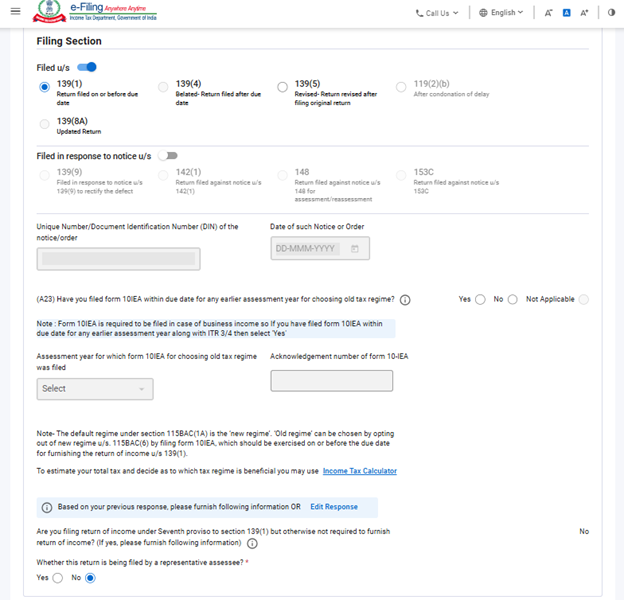

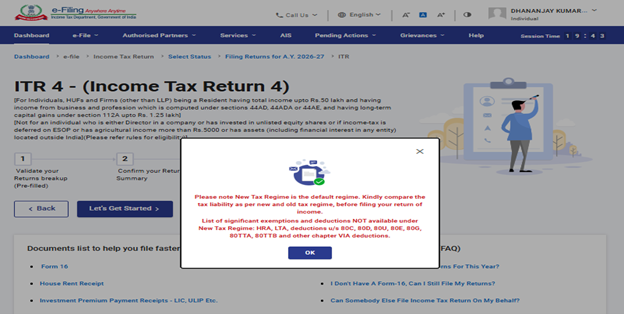

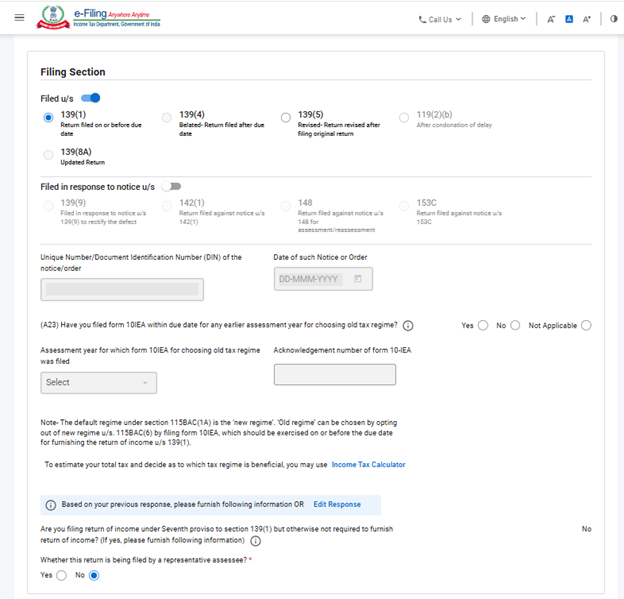

The Finance Act, 2024 has inserted Section 115BAC(1A) to make new tax regime the default tax regime for the assessee being an Individual, HUF, AOP (other than co-operative society), BOI whether incorporated or not, or an artificial judicial person. If an assessee does not want to pay tax according to the New tax regime, it will have to explicitly opt out of it and choose to be taxed under the old tax regime.

An assessee having income from a business or profession can opt out of the new tax regime and switch to the old tax regime for a relevant year. However, with business or profession income, assessee will not be eligible to choose between the two regimes every year. Once assessee has opted out of new tax regime after filing Form 10-IEA, there is only one chance to re-enter into the new tax regime next year Once assessee switches back to the new regime, then again changing tax regimes options will not be available for any succeeding years

However, it must exercise this option of opting out Form No. 10-IEA on or before the due date for filing the return of income under Section 139(1).

- In case of firms this question is not applicable so please select “Not Applicable”.

- If you have opted out of New Tax Regime in any previous year and wish to continue with the same tax regime option in AY 2026-27 then select question “Have you furnished form 10IEA for re-entering in new tax regime in current assessment year?” response as ‘No’ in the ITR.

- If you have opted out of New Tax Regime in any previous year and do not wish to continue to opt out of new tax regime in AY 2026-27 then select question “Have you furnished form 10IEA for re-entering in New Tax regime in current assessment year? ” response as ‘Yes’ and file Form 10-IEA again to re-enter into the new tax regime in 2026-27

- Form 10-IEA is required to file within the due date of filing the return u/s 139(1) of Income Tax Act, 1961

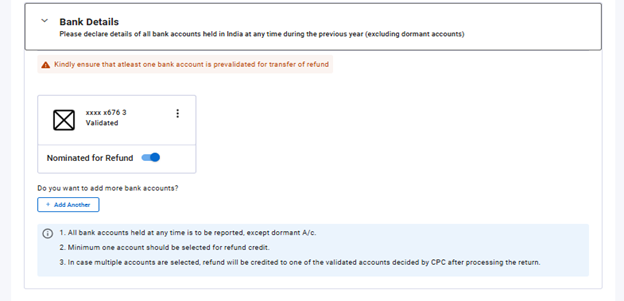

Bank Details:

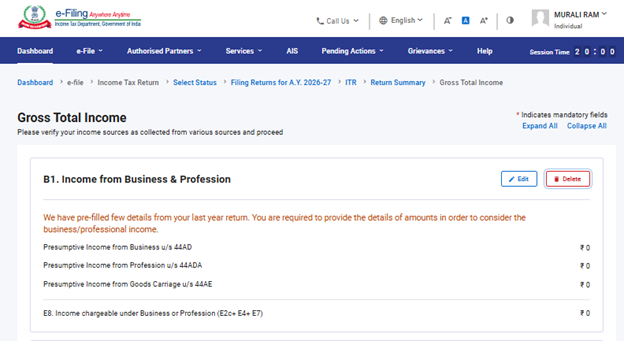

4.2 Gross Total Income

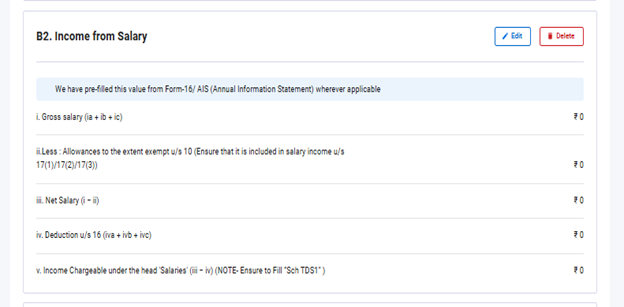

In the Gross Total Income section, you need to review the pre-filled information and verify your income source details from salary / pension, house property, business or profession and other sources (such as interest income, family pension, etc.). You will also be required to enter the remaining / additional details if any.

Income From Salary:

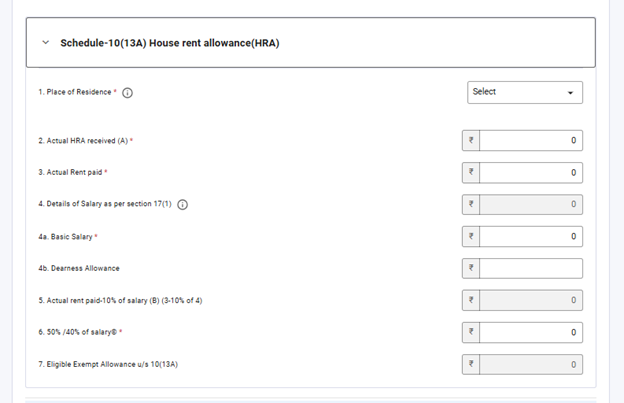

Additional Information for claiming HRA exemption u/s 10(13A):

Income From Business or Profession:

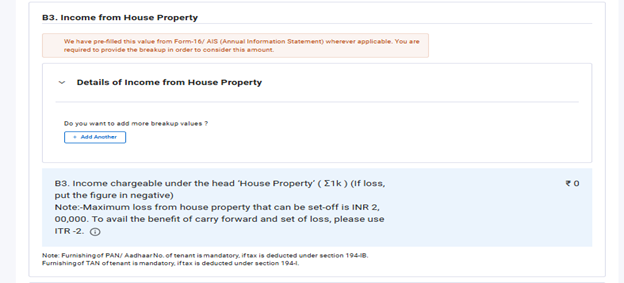

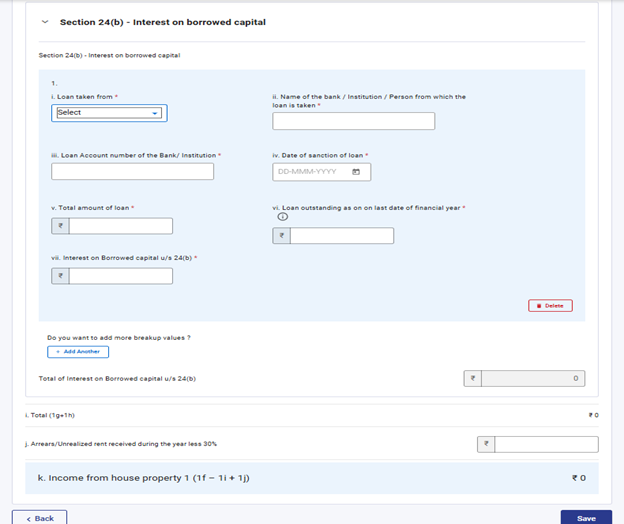

Income from upto two House Property and details of interest on borrowed capital:

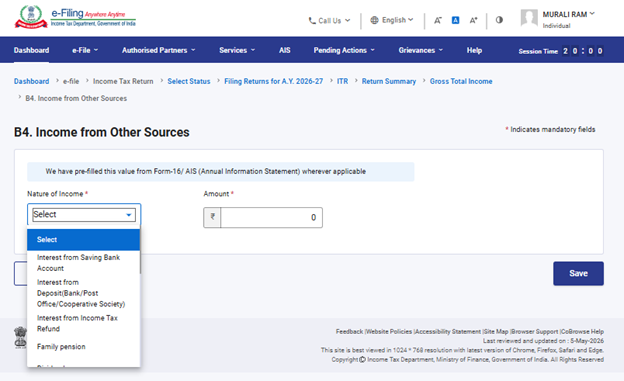

Income from Other Sources:

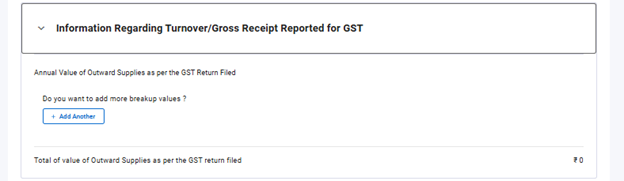

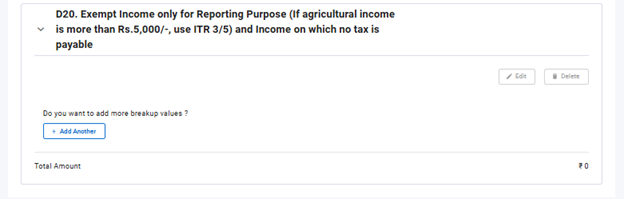

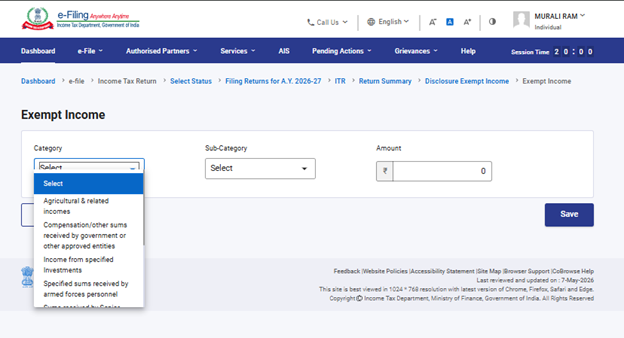

4.3 Disclosures and Exempt Income

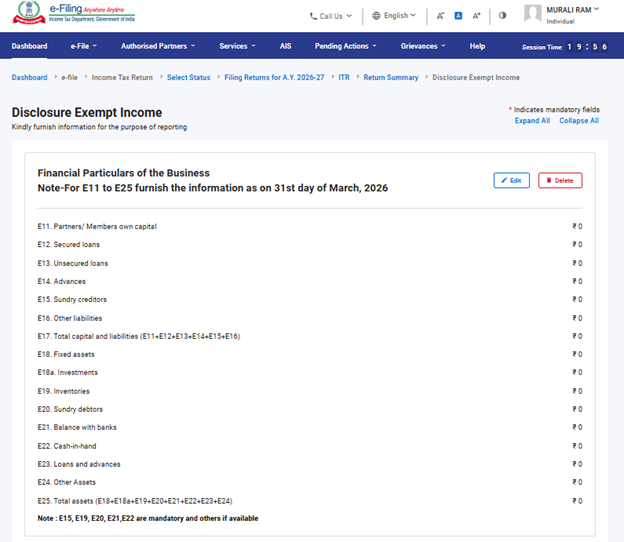

In the Disclosures and Exempt Income section, you need to provide details of financial particulars related to business, information regarding gross receipts reported for GST (Optional) and exempt income.

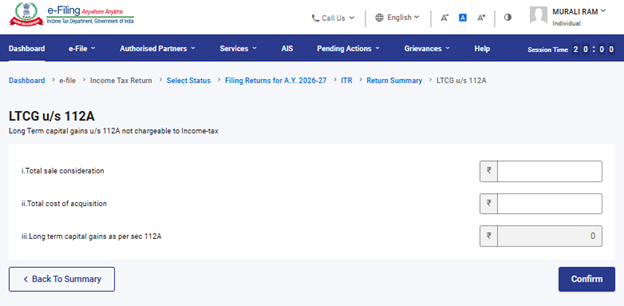

4.4 Long Term capital gains u/s 112A:

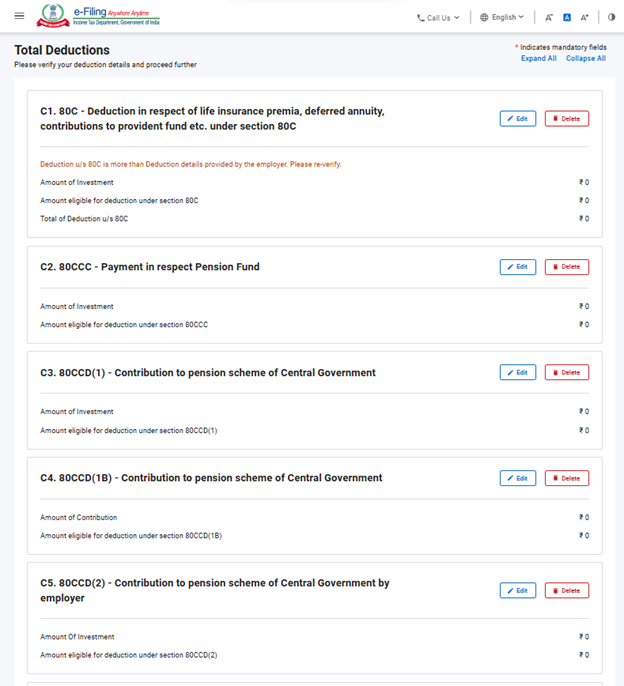

4.5 Total Deductions

In the Total Deductions section, you need to add and verify any deductions you need to claim under Chapter VI-A of the Income Tax Act,1961.

Note: From AY 2025-26 you need to provide some additional information for claiming deductions.

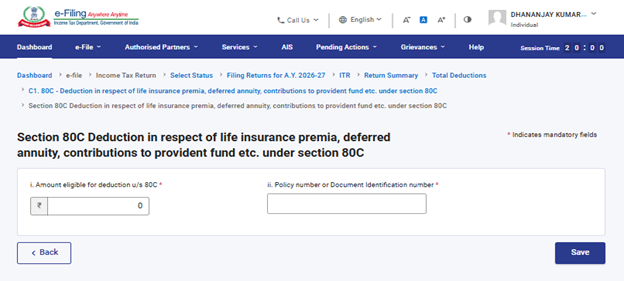

Section 80C:

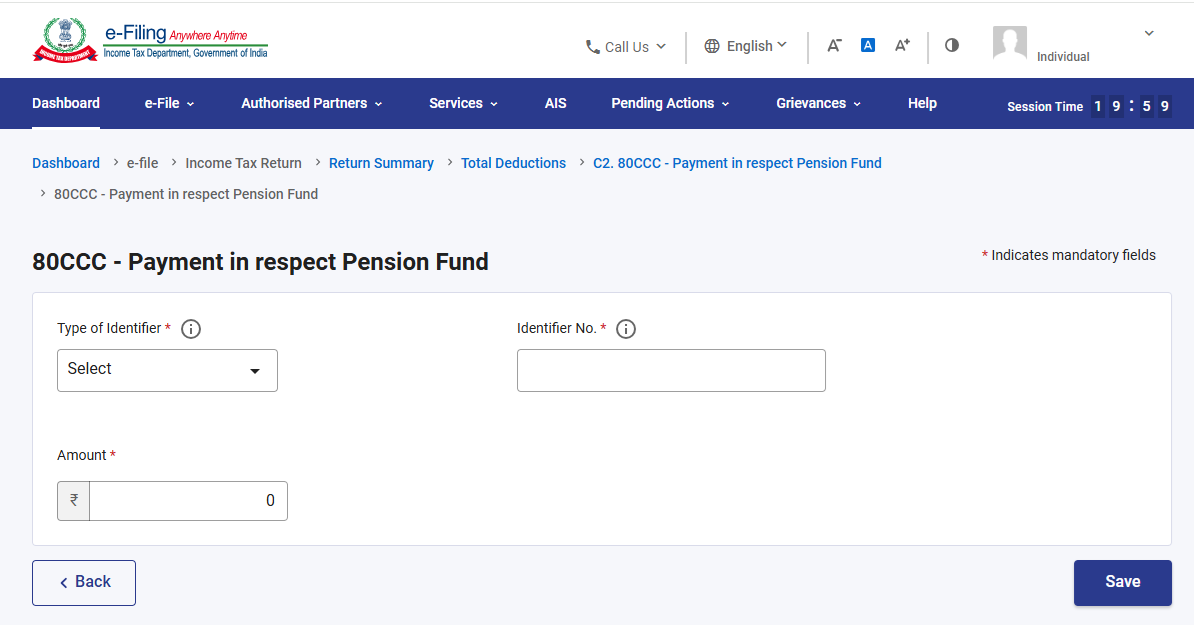

Section 80CCC:

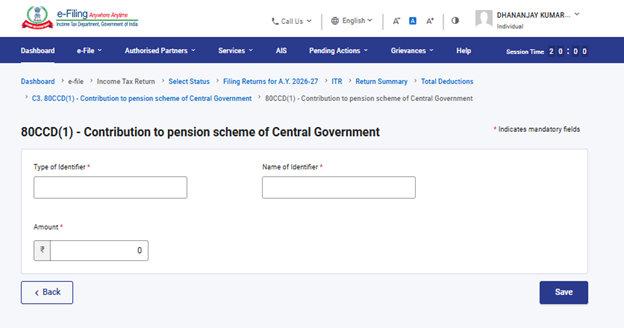

Section 80CCD (1) and 80CCD(1B):

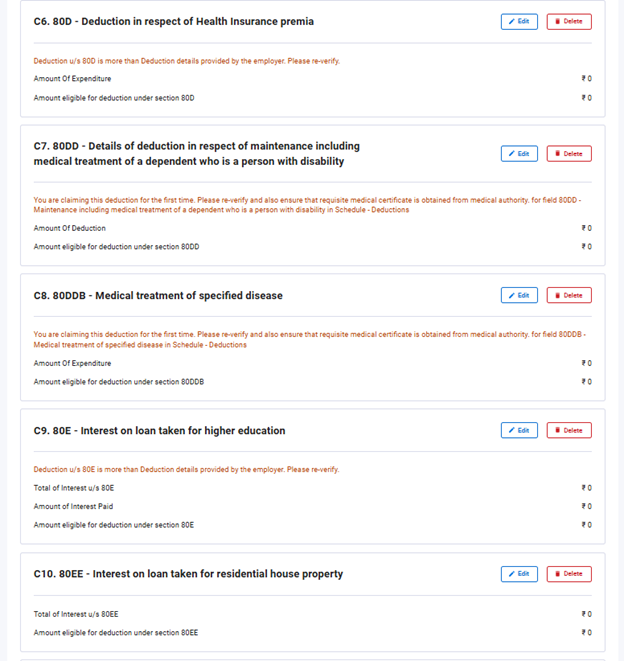

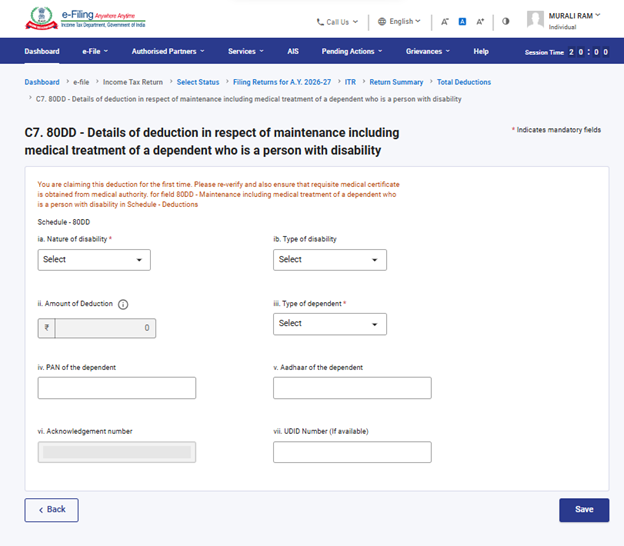

Section 80DD:

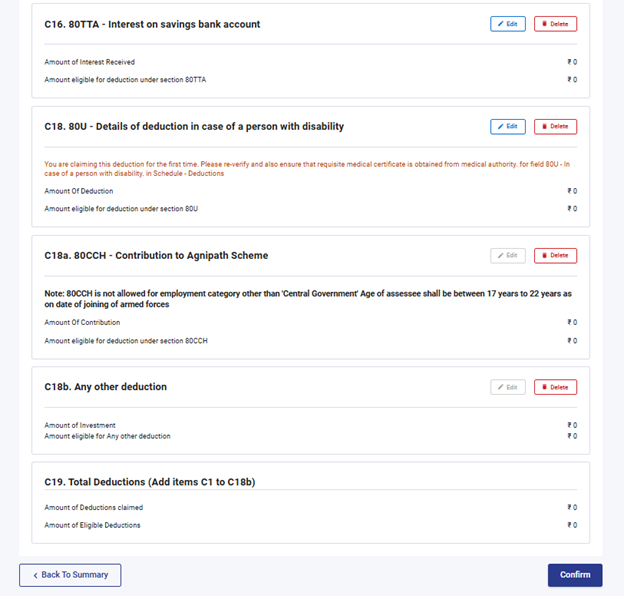

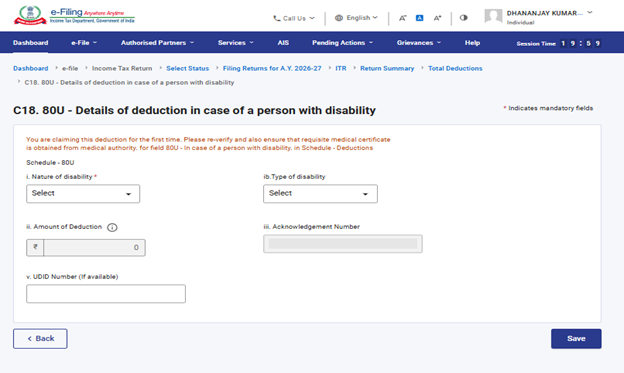

Section 80U:

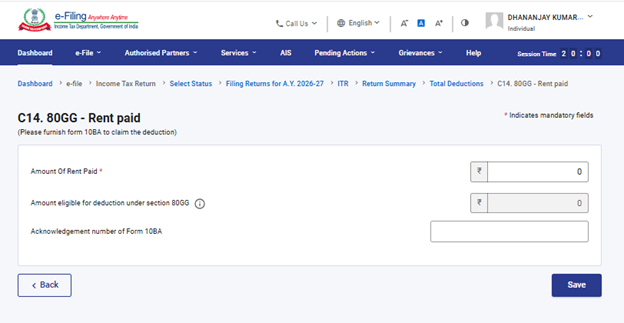

Section 80GG:

Please Note:

1. If you have not opted for Old Tax Regime, only Deductions under Section 80CCD (2)- Employers Contribution to Tier-1 NPS Account and Section 80CCH- amount deposited in the Agniveer Corpus Fund will be enabled.

2. If taxpayers are opting old Tax regime and claiming deduction for autism, cerebral palsy or multiple disabilities u/s 80DD or 80U then it’s Mandatory to file form 10-IA before filing of return.

3. If taxpayers are opting old Tax regime and claiming deduction for u/s 80GG then it’s Mandatory to file form 10BA before filing of return.

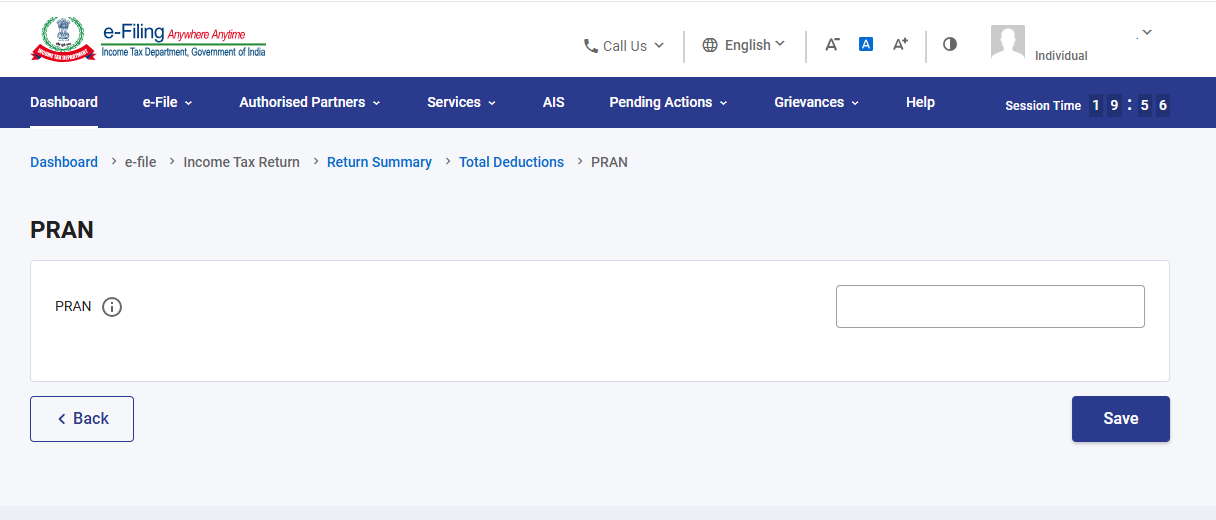

4. PRAN is mandatorily required to claim deduction under 80CCD (1) and 80CCD(1B)

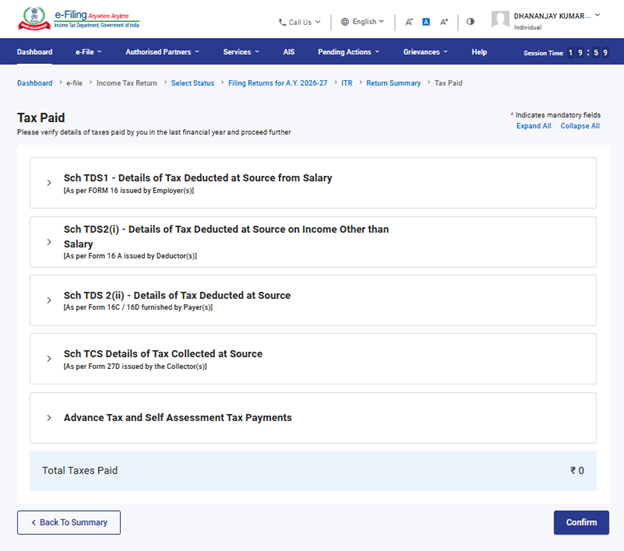

4.6 Taxes Paid

In the Taxes Paid section, you need to verify taxes paid by you in the previous year. Tax details include TDS from Salary / Other than Salary as furnished by the Payer, TCS, Advance Tax, and Self-Assessment Tax.

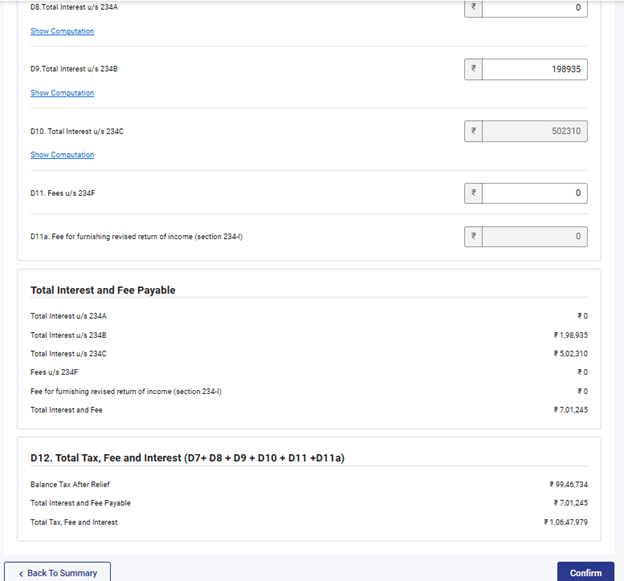

4.7 Total Tax Liability

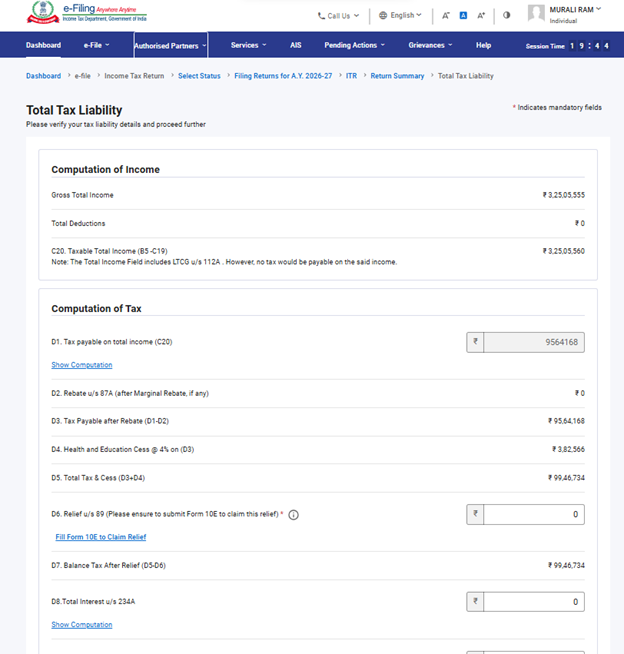

In the Total Tax Liability section, you will be able to view your computation of income, computation of tax, and total tax, cess and interest. You need to check your tax liability details as per the sections you filled previously in the computation of tax section.

5. How to Access and Submit ITR 4

You can file and submit your ITR through following methods:

• Online Mode

• Offline Mode

Follow the steps below to file and submit the ITR through online mode:

Step 1: Log in to the e-filing portal using your user ID and password.

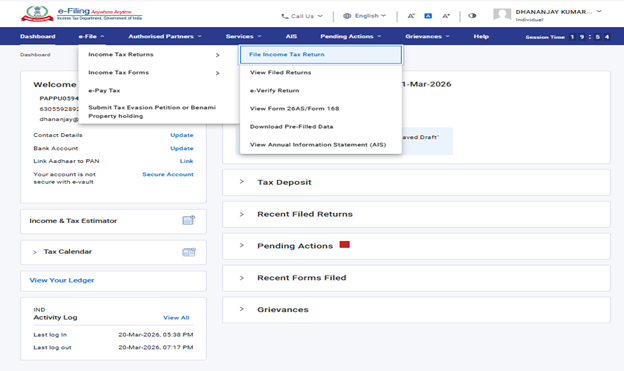

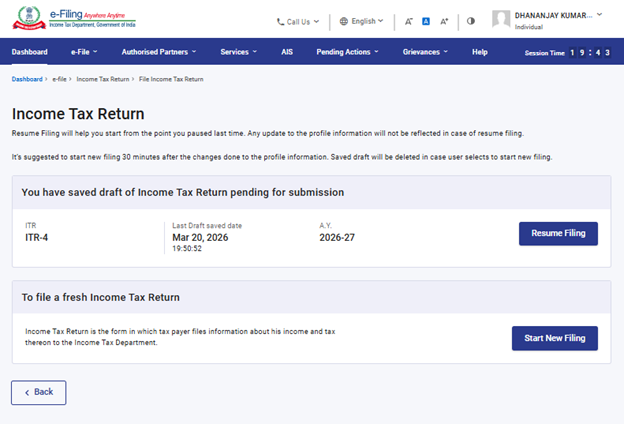

Step 2: On your Dashboard, click ‘e-File’ > ‘Income Tax Returns’ > ‘File Income Tax Return’.

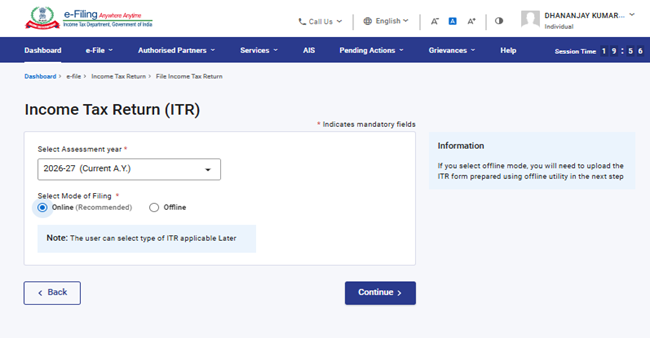

Step 3: Select the Assessment Year as 2026-27 and Mode of Filing as Online and click ‘Continue’.

Step 4: In case you have saved draft of return and it is pending for submission, click Resume Filing. In case you wish to discard the saved draft of return and start preparing the return afresh, click ‘Start New Filing’.

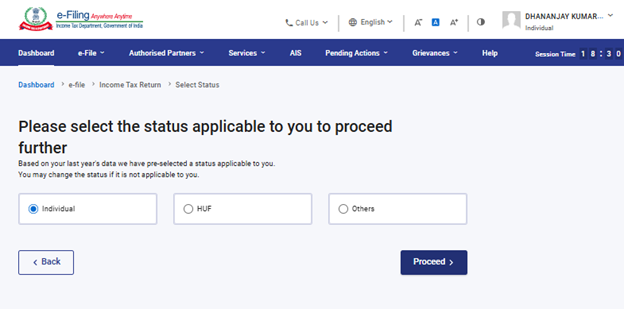

Step 5: Select Status as applicable to you and click ‘Proceed’.

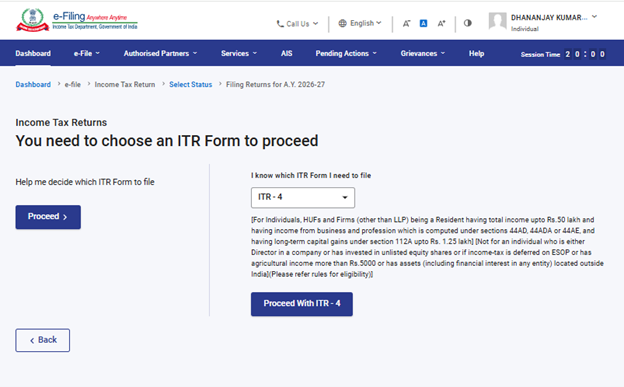

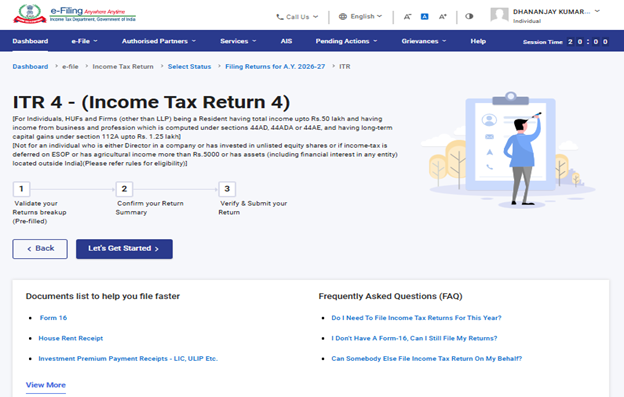

Step 6: Select the ITR-4 form from the dropdown and click ‘Proceed with ITR-4’. If you do not know which ITR form is applicable to you, click on left hand side Proceed button for wizard-based return filing.

Step 7: Once you have selected the ITR applicable to you, note the list of documents needed and click on ‘Let’s Get Started’.

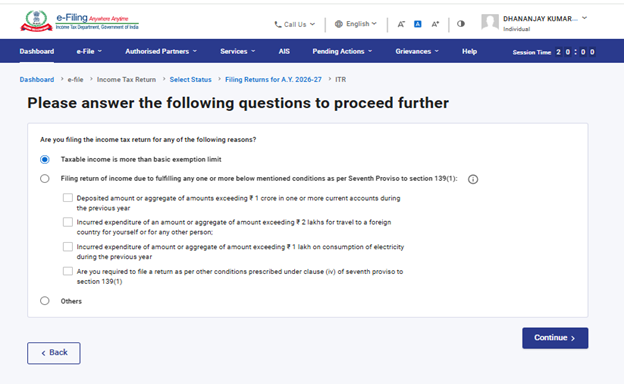

Step 8: Select the reason for filing ITR and click ‘Continue’.

Step 9: Review your pre-filled data in ITR form and edit it if necessary. Enter the remaining / additional data (if required) and click ‘Confirm’ at the end of each section.

Note:

The Finance Act, 2024 has inserted Section 115BAC(1A) to make new tax regime the default tax regime for the assessee being an Individual, HUF, AOP (other than co-operative society), BOI whether incorporated or not, or an artificial judicial person. If an assessee does not want to pay tax according to the new tax regime, it will have to explicitly opt out of it and choose to be taxed under the old tax regime.

An assessee having income from a business or profession can opt out of the new tax regime and switch to the old tax regime for a relevant year. However, it must exercise this option in Form No. 10-IEA on or before the due date for filing the return of income under Section 139(1).

Note:

• If you have opted out of New Tax Regime in Assessment year 2025-26: Select “Yes, No or Not Applicable”. If yes is selected, then Enter the Date of filing and acknowledgement No. of Form 10-IEA filed.

• If you have selected No or NA for AY 2025-26 and want to opt out of New Tax Regime for Current Assessment year 2026-27: Select “Yes”, otherwise select “No”. If yes is selected, then Enter the Date of filing and acknowledgement No. of Form 10-IEA filed.

Step 10: Enter your income and deduction details in the different sections of ITR form. After completing and confirming all the sections of the form, click ‘Proceed to Verification’.

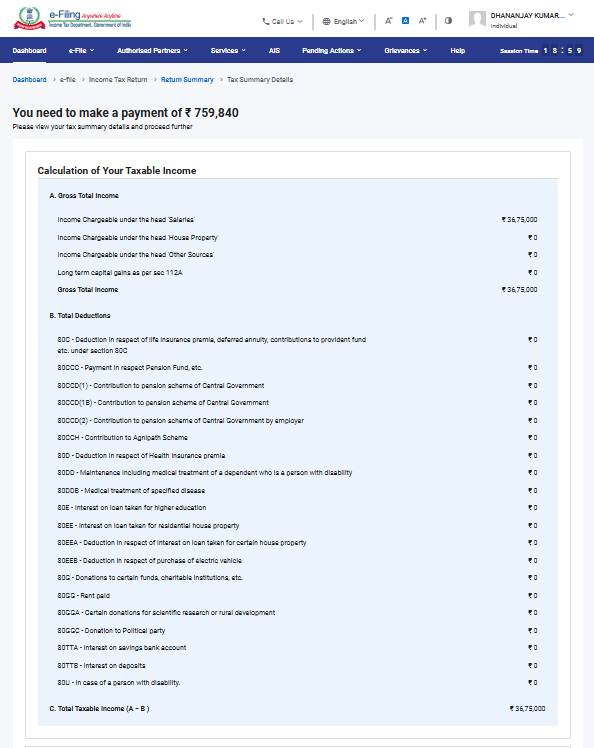

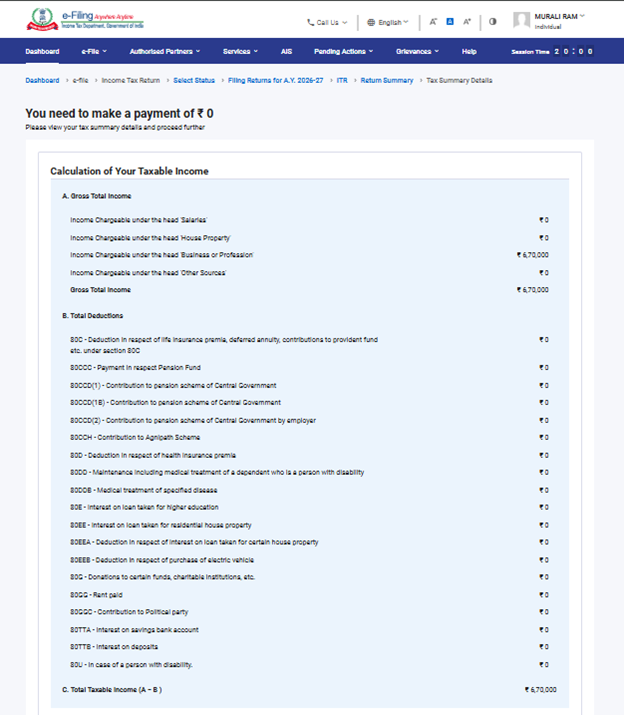

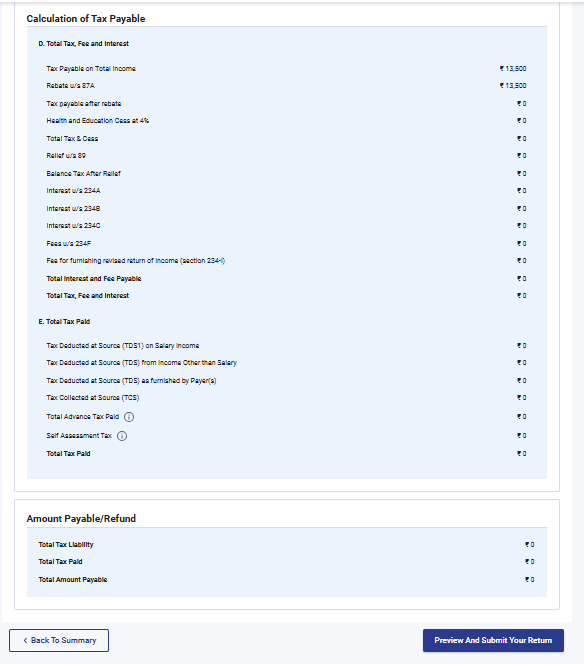

Step 11: In case there is a tax liability

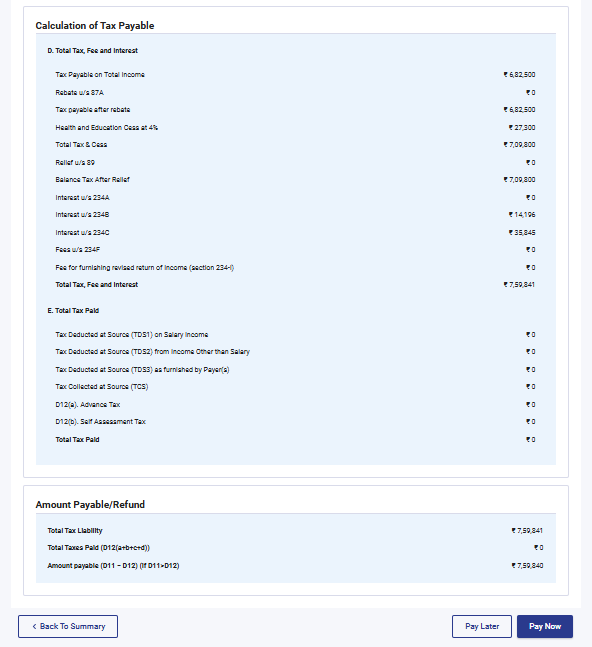

You will be shown a summary of your tax computation based on the details you provided. If there is tax liability payable based on the computation, you will get the Pay Now and Pay Later options at the bottom of the page. It is recommended to use Pay Now option.

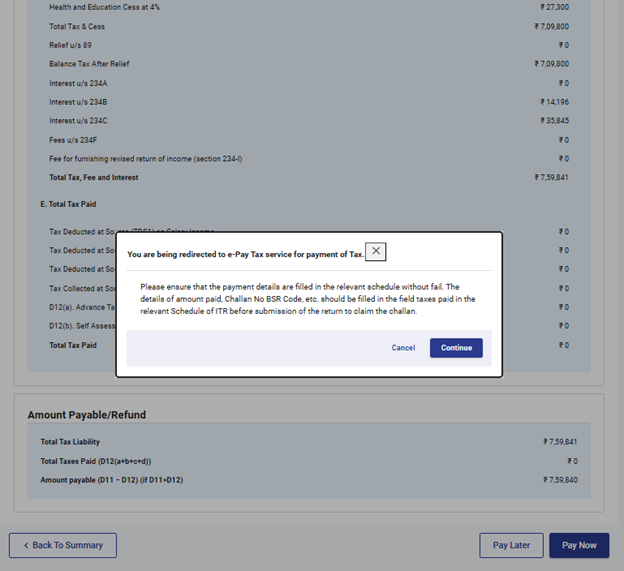

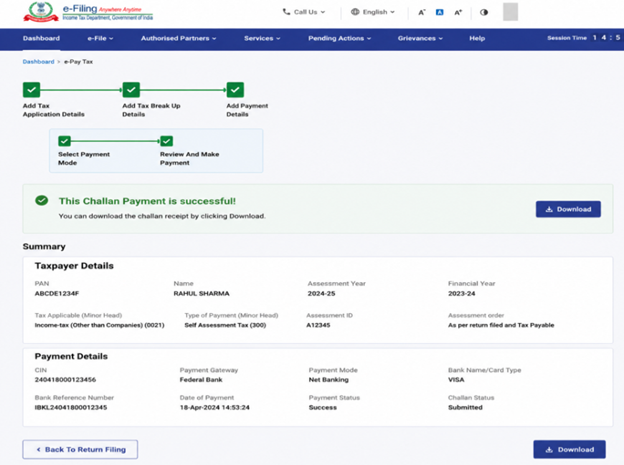

Step 11a(i): If you click on “Pay Now” you will be redirected to e-pay Tax service. Click ‘Continue’.

• Note: You will be taken to e-Pay Tax page on the portal to make tax payment after you click Continue. Refer to e-Pay Tax user manuals to learn more.

Step 11a(ii): After successful payment through e-filing portal, a success message is displayed. Click 'Back to Return Filing' to complete filing of ITR.

• If you opt to Pay Later, you can make the payment after filing your Income Tax Return, but there is a risk of being considered as an assessee in default, and liability to pay interest on tax payable may arise.

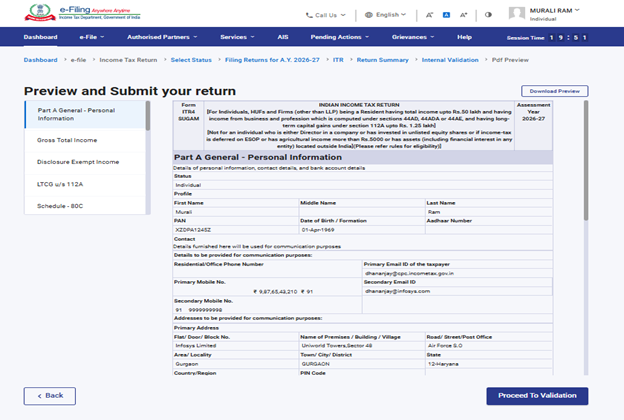

Step 12: If there is no tax liability payable, or if there is a refund based on tax computation, you will be taken to the ‘Preview and Submit your Return’ page.

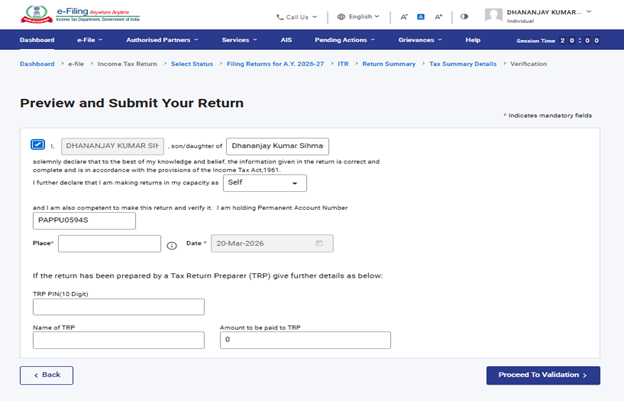

Step 13: On the Preview and Submit Your Return page, name and other details will be auto populated. Select the declaration checkbox, Enter the Place and click ‘Proceed to Validation’

Note: If you have not involved a tax return preparer or TRP in preparing your return, you can leave the textboxes related to TRP blank.

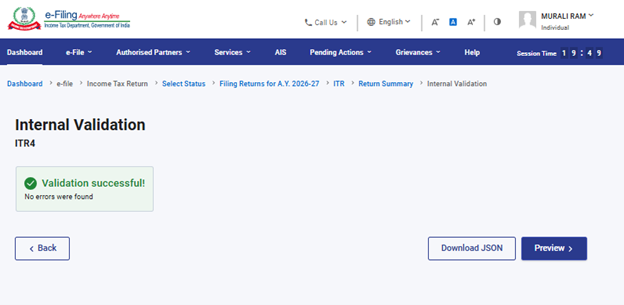

Step 14: Once Internal validation is successful, click on ‘Preview’.

Note: If you are shown a list of errors in your return, you need to go back to the form to correct the errors. If there are no errors, you can proceed to Preview your return.

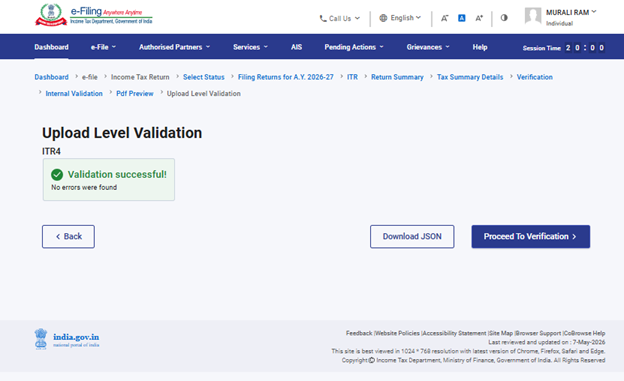

Step 15: On Preview of Return page click ‘Proceed to Validation’.

Step 16: Once validated, click ‘Proceed to Verification’.

Note: You will be shown a list of validation errors in your return, if any. You need to go back to the form to correct the errors. If there are no errors, you can proceed to e-Verify your return by clicking ‘Proceed to Verification’.

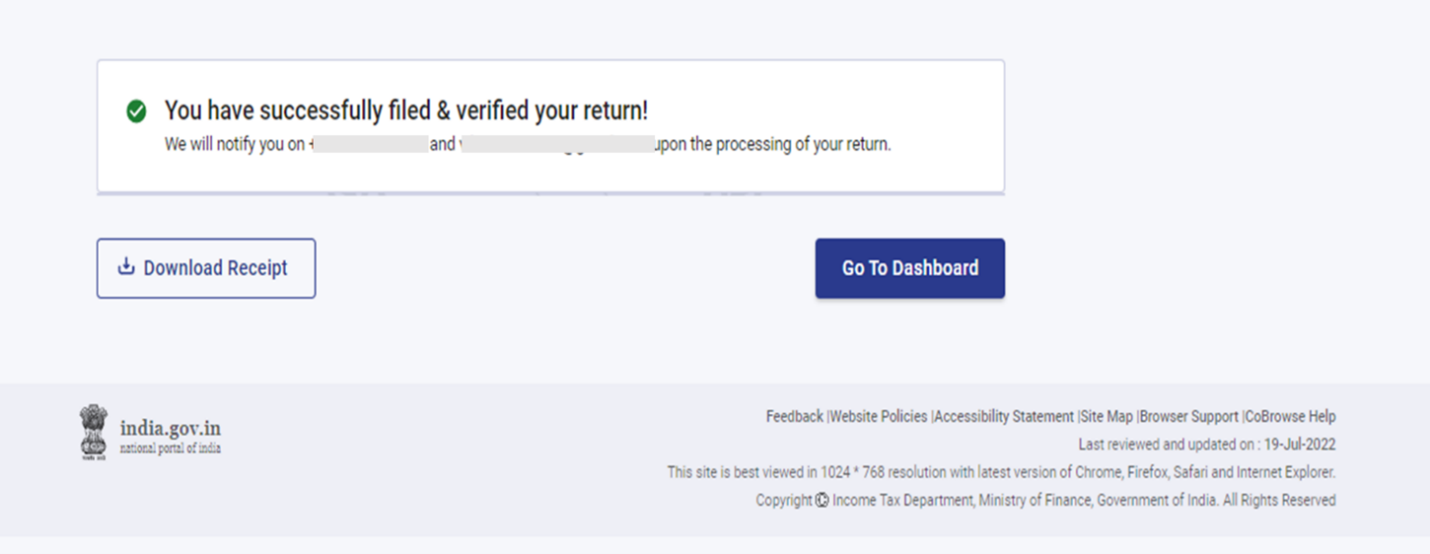

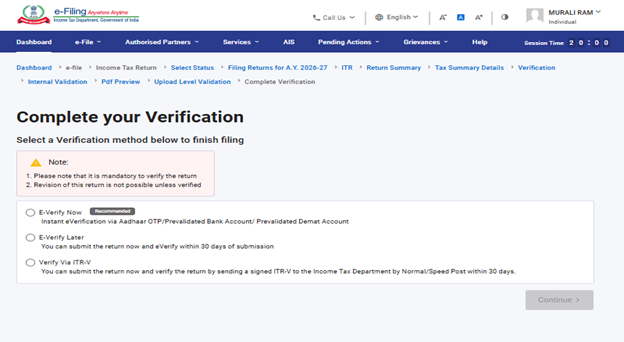

Step 17: On the ‘Complete your Verification’ page, select your preferred option and click ‘Continue’.

It is mandatory to verify your return, and e-Verification (recommended option – e-Verify Now) is the easiest way to verify your ITR – it is quick, paperless, and safer than sending a signed physical ITR-V to CPC by speed post.

Note: In case you select E-Verify Later, you can submit your return, however, you will be required to verify your return within 30 days of filing of your ITR.

Step 18: On the E-Verify page, select the option through which you want to e-Verify the return and click ‘Continue’.

Note:

• Refer to How to e-Verify user manual to learn more.

• If you select Verify via ITR-V, you need to send a signed physical copy of your ITR-V to Centralized Processing Center, Income Tax Department, Bengaluru 560500 by speed post within 30 days.

• Please make sure you have pre-validated your bank account so that any refunds due maybe credited to your bank account.

• Refer to My Bank Account user manual to learn more.

Please Note: As per Notification No. 2 of 2024 dated 31/03/2024-

1. Where the return of income is uploaded and e-verification/ITRV is submitted within 30 days of uploading – In such cases the date of uploading the return of income shall be considered as the date of furnishing the return of income.

2. Where the return of income is uploaded but e-verification or ITR-V is submitted after 30 days of uploading – In such cases the date of e-verification/ITR-V submission shall be treated as the date of furnishing the return of income and all consequences of late filing of return under the Act shall follow, as applicable.

3. The duly verified ITR-V in prescribed format and in the prescribed manner shall be sent either through ordinary or speed post or in any other mode to the following address only:Centralized Processing Centre, Income Tax Department, Bengaluru - 560500, Karnataka.

4. The date on which the duly verified ITR-V is received at CPC shall be considered for the purpose of determination of the 30-day period from the date of uploading of return of income.

5. It is further clarified that where the return of income is not verified after uploading within the specified time limit such return shall be treated as invalid.

Once you e-Verify your return, a success message is displayed along with the Transaction ID and Acknowledgment Number. You will also receive a confirmation message on your mobile number and email ID registered on the e-filing portal.